Option Analysis Setups: Do or Die for $SPY & Tech Vulnerabilities

It's all about the FOMC

Market Abstract:

A Weak close to Friday + end of month created new YTD lows. Meanwhile the inversely correlated VIX did not print new YTD highs. Selling was moreso concentrated in single tickers vs index level. Overall, weak liquidity is not helping, but there may be a silver lining in all this.

Why? Let’s recap and build up to the key point.

The S&P 500 started the week having closed on the prior week’s low. Rallies were short lived and unstable, which is to be expected when the share volumes or long calls aren’t leading the charge. Instead, it was mostly put selling on the weekly lows that induced short term rallies, and then calls being sold at the highs near 430 every time it hit this week (Monday, Tuesday, Thursday).

So, share volume at the index level has been low (which = no real money macro buyers), calls are not being bought in size past the FOMC, and not at higher prices (for the most part), and any intraday rallies are mostly due to short dated puts being sold. Oh, and did I mention option strikes keep ‘laddering’ down, which is a bearish signal as traders accept the new/lower prices.

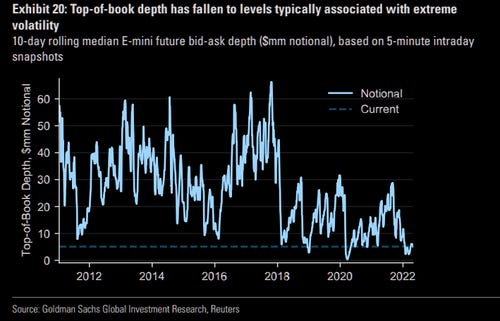

None of this creates a bull market, nor a sustained rally that lasts more than 2 days. On top of this, the liquidity in the ES has been low, so when selling occurs, it takes away liquidity, and exacerbates the rally (Image below).

All of this should paint a potentially ominous signal, and you’d be within the bounds of sanity to think such a line.

However, there is a silver lining.

While traders are going to hold insurance (long puts) heading into the FOMC, we have a heavily put dominated market. But…and this is an important but…VIX didn’t burst out to new highs.

This matters because the higher VIX goes, the more energy (long VIX calls/futures) it needs to maintain its high prices. But…higher IV/VIX means less people are willing to buy at these levels. So unless it finds fresh meat (new buyers of long VIX calls/futures, more long put buying), it becomes more fragile at the thinner atmospheric levels.